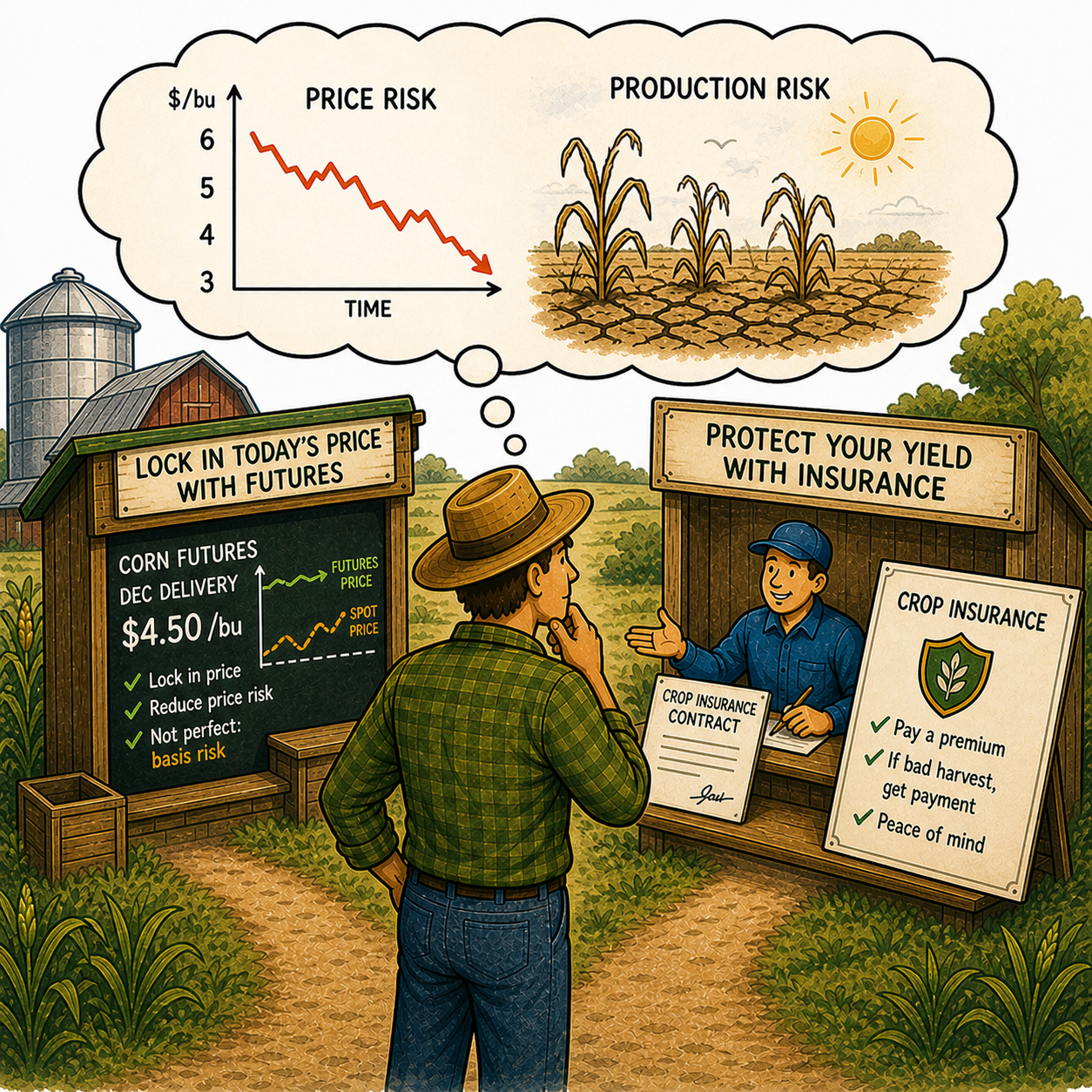

class: center, middle, inverse, title-slide .title[ # Agricultural Markets ] .subtitle[ ## Lecture 9: Risk and Insurance ] .author[ ### David Ubilava ] .date[ ### University of Sydney ] --- # Uncertainty and risk .pull-left[  ] .pull-right[ - Because of complexities of physical and economic systems in agriculture, most processes that consumers of agricultural commodities care about unfold with some degree of *uncertainty*. - Uncertainty means that any given action can lead to many possible outcomes. - A decision-making under uncertainty is characterized by *risk*, as not all possible consequences are equally desirable. ] --- # Risk aversion .right-column[ - Uncertainty in agricultural markets (or any markets, for that matter) is an issue because a typical person is *risk-averse*. - A person is said to be risk-averse if, for every lottery `\(F(w)\)`, where `\(w\)` is realized wealth, they will always prefer (at least weakly) the certain amount `\(E(w)\)` to the lottery itself; that is: `$$U\left[\int w dF(w)\right] \ge \int U(w)dF(w).$$` - A simplified discrete variant of the foregoing is that a risk-averse person would prefer a guaranteed pay-out of $100 rather than a pay-out of either $0 or $200 each with probability of 50%. ] --- # Absolute vs relative risk aversion .right-column[ - Under the assumption of monotonically increasing concave utility function, `\(U(w)\)`, we can have *absolute risk aversion*, `$$A(w) = -U''(w)/U'(w),$$` and *relative risk aversion*, `$$R(w) = wA(w).$$` - Assuming that people become less averse to a gamble as their wealth grows, `\(A(w)\)` can be seen as a decreasing function of `\(w\)`; however, typically there are no *a priori* expectations regarding any particular behavior of `\(R(w)\)` with respect to `\(w\)`. ] --- # Uncertainties faced by farmers .right-column[ - An agricultural producer faces risks related to * Prices: production decisions are made far in advance of realizing the output and prices. * Production: agricultural production heavily relies on exogenous factors, such as weather, which can be important source of idiosyncratic uncertainty. * Technology: technological advancement may make quasi-fixed investments obsolete. * Policy: government, through its policies, plays an important role in agriculture, and any changes to these policies creates considerable risk for agricultural investments. ] --- # Intrinsic and instrumental impacts of risk .right-column[ - Risk has *intrinsic* and *instrumental* impacts on farmers. - The intrinsic impacts work through current well-being: people are better off when income and consumption are stable. - Indeed, people's aversion to consumption fluctuations is the basic behavioural motivation for insurance. ] --- # Intrinsic and instrumental impacts of risk .right-column[ - The instrumental impacts of risk are evident in the short-run but their real consequences manifest in the long run. - In response to risk, farmers adjust their behavior. Particularly in lower income countries, farmers are: * reluctant to invest in new technologies or adopt new seed varieties, instead they prefer to grow traditional crops; * diversify their production by planting different crops across spatially separated fields in hopes to mitigate losses. - As a result, they incur extra costs, do not capitalize on economies of scale, and are less efficient overall. ] --- # Managing risk via futures markets .right-column[ - One mechanism to mitigate risk in agriculture is via hedging, which shifts the price risk. The acquisition of a futures contract can help manage risk by assuring (approximately) a given level of returns. - From the standpoint of an *arbitrage hedge*, if the expected convergence of the spot and futures prices at some future time period is sufficient to cover storage costs, an agent can assure the return by hedging. ] --- # Managing risk via futures markets .right-column[ - Another way to look at hedging on futures markets, is its ability to assist a firm in assuring a return from their business activities. - A merchant can make a bid on a contract to export certain amount of commodity, without actually having (enough of) it in possession; or, they can offer farmers forward contracts at planting time to purchase their grain at the harvest. - This is referred to as an *operational hedge*, which can be seen as a temporary substitute for later transactions in the cash market. ] --- # Managing risk via futures markets .right-column[ - Futures markets can assist a producer to price their output before it is produced. Similarly, a processor can also price the input, prior to the actual purchase of the physical commodity. - Thus, an *anticipatory hedge* is based on expected future actions, such as the production and sale of the commodity. An anticipatory hedge can lock in a profit, when price relationships are favorable. ] --- # Futures market failure .right-column[ - Assuring the return by hedging, crucially relies on the assumption of *convergence*. Convergence may not be exact (most of the time it is not). As a consequence, hedges do not give perfect results, which is also known as [basis risk](https://www.cmegroup.com/education/courses/introduction-to-grains-and-oilseeds/learn-about-basis-grains.html). - Thus, basis risk, or our inability to forecast convergence with certainty, poses a problem for hedgers. - Another possible problem is inherent to the production risk: in times of a negative supply shock, a portion of the hedge will turn into a speculative position, which can result in a loss on the position on the futures market. ] --- # Managing risk via insurance .right-column[ - An alternative mechanism to mitigate risk in agriculture, which by no means is a substitute to producers' participation in futures markets, is via crop insurance. - A substantial production (and price) variability has led producers realize the importance of risk management as a component of their expected profit-maximization strategies. - A producer can take control of risk management, or outsource it: * a firm may build up its own funds to cover sudden losses; or * a firm can transfer this risk to an insurer for a fee. ] --- # Managing risk via insurance .right-column[ - Insurance companies are specialized risk bearers that spread the risk over a wide area and groups of people or businesses. - Sometimes, government price- and revenue-supporting programs can serve as a mechanism to mitigate the risk (but availability of such programs vary from country to country). - In fact, while crop insurance markets have existed for a long time in some parts of the world, their existence has depended crucially on government support. ] --- # Managing risk via insurance .right-column[ - Private agricultural insurance markets may fail because the costs of maintaining these markets imply unacceptably low average payouts relative to premiums. - Moreover, the perceived demand for crop insurance may be overstated because farmers have an option to manage the risk individually. ] --- # Managing risk via insurance .right-column[ - General features of insurance programs are that * they are based on historical data; * they can be farm-based or area-based; * indemnity is triggered if the revenue (or yield) falls below some threshold; * a producer needs to pay a fee - premium - to participate in the program. - In addition, the government may choose to subsidize the program. ] --- # Insurance market failures .right-column[ - Two main issues that are associated with crop insurance (or any insurance for that matter) are *moral hazard* and *adverse selection*. - Moral hazard implies that a farmer's optimal decision may be different with insurance as compared to that without insurance. - Adverse selection implies that farmers that choose to insure at a given rate, are also the ones who are more exposed to risk. ] --- # Moral hazard .right-column[ - Moral hazard problems arise, when the insurer contracts on a risk-averse producer whose inputs are unobservable. With or without moral hazard, the contract is designed in such way that a farmer is willing to participate in the program. - Under moral hazard, however, it is no longer optimal for the risk-neutral insurer (principal) to assume all risk; some residual risk must be borne by the risk-averse producer (agent). ] --- # Moral hazard .right-column[ - The implications of the moral hazard problem are not as clear-cut as the intuition might suggest. - On the one hand, being relieved of some of the consequences of low input use, the producer may reduce input intensity. - On the other hand, if input use is risk-increasing, then a high-risk environment may cause the producer to use fewer inputs than a low-risk environment. ] --- # Adverse selection .right-column[ - When the insurer is not completely informed about the nature of the risk being insured, then the insurer faces the problem of adverse selection. - Avoiding adverse selection may require the successful crop insurance program to identify, acquire, and skilfully use data that discriminate among different risks. - While costly to implement, such data management procedures may be crucial because, unless rates are perceived as being acceptable, the market may collapse. ] --- # Adverse selection .right-column[ - Identifying a sufficiently large number of relatively homogeneous risks is a prerequisite for a successful contract. - Another factor that can facilitate to sustain the contract is sufficiently high degree of risk-aversion among producers. ] --- # Moral hazard vs adverse selection .right-column[ - While moral hazard and adverse selection are conceptually distinct phenomena, they share information asymmetry as a common characteristic feature. - The difference between these can be subtle: > Consider a corn and soybeans farmer who has one hectare of high quality land and one hectare of low quality land. Given the decision to insure corn but not soybeans, the planting of soybeans on the poor quality land is moral hazard. Given the decision to plant soybeans on poor quality land, the insuring soybeans is adverse selection. ] --- # Mitigating the insurance market failure .right-column[ - Due to the informational nature of main barriers to successful crop insurance markets, the obvious solution is to facilitate better (ideally, complete) information. - One approach to reduce adverse selection is to obtain and use farm-level (rather than area-level) information; but this creates incentives for moral hazard. - Alternatively, area yield insurance can solve moral hazard and possibly mitigate adverse selection, but this will not completely alleviate the production risk. ] --- # Mitigating the insurance market failure .right-column[ - Revenue insurance, instead of yield insurance, mitigates somewhat the incidence of moral hazard and adverse selection. - It also serves the main purpose of crop insurance as it addresses the issue of income risk facing producers. ] --- # Mitigating the insurance market failure .right-column[ - Another crop insurance mechanism, that can mitigate some of the aforementioned issues, is the index-based insurance, also referred to as *weather derivatives*. - Weather derivatives are based on historical weather data of the area where the farm is located. - Indemnity is triggered if weather conditions are considerably worse than the historical normal. - This works because weather is intrinsically linked with agriculture. - Correlation between weather and yields is not perfect, however. In instances when it's weak (e.g., a farm located far from a weather station), the index-based insurance loses its appeal. ] --- # Readings .pull-left[  ] .pull-right[ Tomek & Kaiser, Chapter 11 ("Government Intervention in Pricing Agricultural Products") & 13 (until "Price Discovery") Norton, Alwang & Masters, Chapter 14 ("Finance, Risk, and Insurance") ]